Metrocity Finance

Jaipur

Very good software. Supportive staff. value for money. Using software for the last nine years. Satisfied with software and after sales support.

Metrocity Finance

Jaipur

Very good software. Supportive staff. value for money. Using software for the last nine years. Satisfied with software and after sales support.

Sidharth Prabhu

Swagat HFC, Mumbai

We migrated to Jaguar Software LOS & LMS in 2019 and it's been more than 5 years of association. The team helped us at all instances with the initial migration process seamlessly.

Sunil Kumar

Setia Autofinance, Jaipur

We are using Jaguar Cloud 360 for almost a year, it is an exceptionally good and user-friendly software for NBFC. It provides complete end to end solution including accounting.

Metrocity Finance

Jaipur

Very good software. Supportive staff. value for money. Using software for the last nine years. Satisfied with software and after sales support.

Sidharth Prabhu

Swagat HFC, Mumbai

We migrated to Jaguar Software LOS & LMS in 2019 and it's been more than 5 years of association. The team helped us at all instances with the initial migration process seamlessly.

Sunil Kumar

Setia Autofinance, Jaipur

We are using Jaguar Cloud 360 for almost a year, it is an exceptionally good and user-friendly software for NBFC. It provides complete end to end solution including accounting.

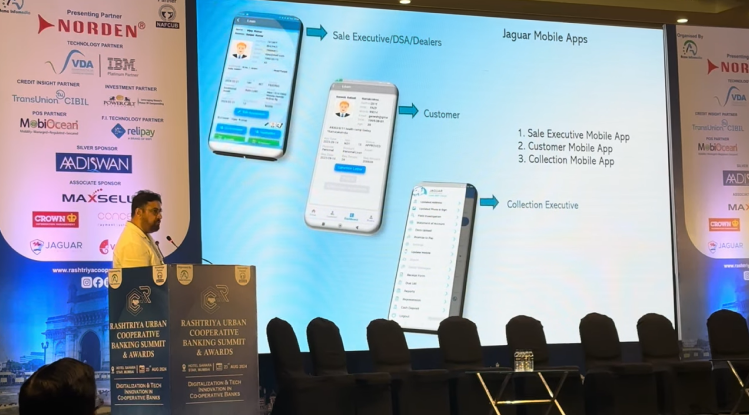

Introducing Jaguar 360° Cloud - A robust digital lending platform which is customizable to the clients processes creating a unique proposition. It is an end to end lending solution covering all loan verticals and is running successfully with a PAN India presence and especially with approximately 90% Companies in the north. Companies like "Au Financiers" grew to a size of 3500 crore on our software.

Using BPM flowcharting we are able to quickly revamp our platform to meet the client processes and procedures within a matter of minutes. Clients will have faster GTM strategy as any of the loan verticals can be activated within a couple of days should the client decide to launch a new lending line.

Know More

Why Choose Jaguar Software India

Our founders are ex-lenders, and they understand the lenders in the financial industry. With in-depth subject matter expertise and strong technical capability in software design and development, Jaguar was able to architect effective and operational products for the lending ecosystem.

How - Design Thinking

With a decade of product design experience and having co-planned with more than 200+ Lenders, including new-age Small Finance Banks, our team could co-design intelligent lending solutions.

After spending more than 10 months evaluating modern technologies, our team was able to create a flexible and scalable design architecture from scratch - while enabling an unparalleled User Experience (UX) and intuitive User Interface (UI).

What - ERP++ Solution

Jaguar 360 Cloud is an ERP effort - it is an ERP++ solution for lenders supporting 360° business management.

It is a flexible digital canvas product where lenders are empowered to create their products, define their workflows, and automate their processes with full visibility and transparency. Our goal is to help our customers achieve 10 times productivity improvement, and sometimes higher!

Our Product maturity is time tested with over 20 years of experience and 150+ satisfied lender clients across NBFCs, Banks, HFCs, FinTechs, and MFIs, stemming from the fact that the founders themselves ran a successful NBFC which was started by Wg. Cdr. PPS Bains and hence the name JAGUAR.

Know MoreWhy 150+ lenders choose us

Designed by engineers with deep domain expertise and first-hand experience of NBFC operations. We have keen awareness of changing market challenges and are actively involved in finance company associations.

We're dedicated to customer success and focus on solving all customer challenges. Over the years, this has led to very comprehensive solutions. Given our domain expertise, we're able to design simple...

We're committed to keeping our solutions up to date with the latest technology and deployment models. We have developed Cloud based Digital Lending solution to turn all traditional lenders into Fintechs.

We have Clients ranging from startups to mid sized. At the highest end, our solutions are lightweight and scalable, and are already supporting upto 10,000 new loans a month With scalability to much higher...

Complete digital Customer onboarding digital credit and underwriting with BPM Workflow flowcharting based products design. Perhaps the most flexible and modern solution With unmatched scalability

We accompany you throughout the process of digital transformation.

Close collaborations enabled the growth of operations to 3500 crore on our software platform, which is a successful case of innovation and collaboration in the context of AU Small Finance Bank.

Collaborating since 2017, Akasa Finance has increased its portfolio by ₹800 to 1300 crore, with our software to make their operations more efficient and scalable.

Our complete loan management solutions have seen Aasaan Loan increase its portfolio from 2018, 500 crore to 1,000 crore.

The collaboration since 2002 has helped Punjab Kashmir Finance to conduct its business of over 500 crore loans and deposits on a strong, reliable platform.

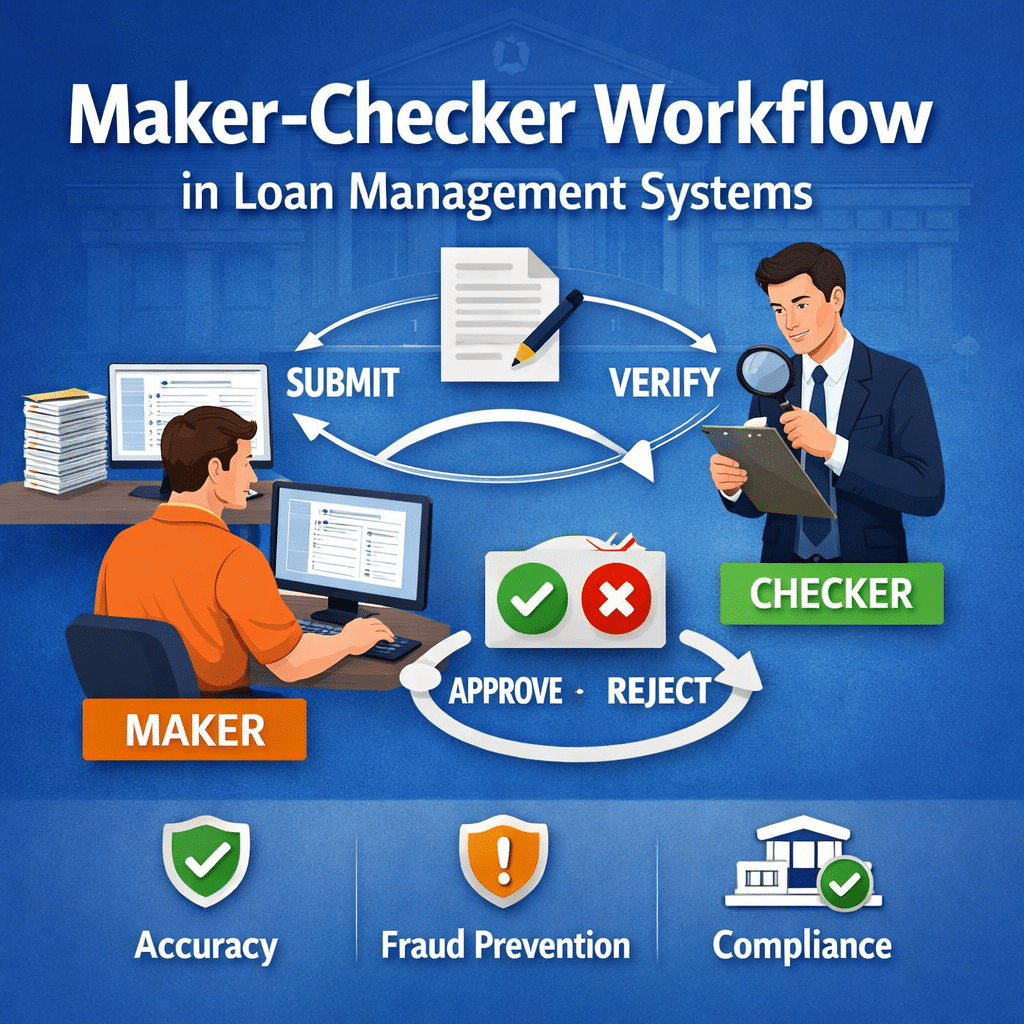

We have complete logging feature as per banking standards, as required by RBI from 1 April 2023.