The NBFC companies in India are fast changing, and technology is the central nerve of this evolution. If you have ever applied for a personal loan or shopped around for financial products online, chances are that you’ve personally seen this transformation. Just a few years ago, getting anything from a non-bank finance company — such as an instalment loan to pay rent and utilities until your next paycheck or a tax-refund anticipation loan secured by the promise of your return coming in — would have involved piles of paperwork, multiple trips to strip-mall offices and slow, paper-laden systems.

Today, many of these processes are digital and frictionless; in fact, they’re faster than at any point in history — courtesy of technology such as AI, ML data analytics, and API-driven platforms. This transformation is not just enhancing the customer experience but also extending credit to the underbanked segments in Tier-2 and 3 cities, MSMEs and new-to-credit customers. NBFCS that operate in eco-my digital systems are making even more strides versus traditional banks in providing customised products, quicker processing and better risk management -Revamping India’s credit eco-system.

Here in this blog, we provide you with information on how technology is transforming NBFC lending in India. Stay tuned with this blog.

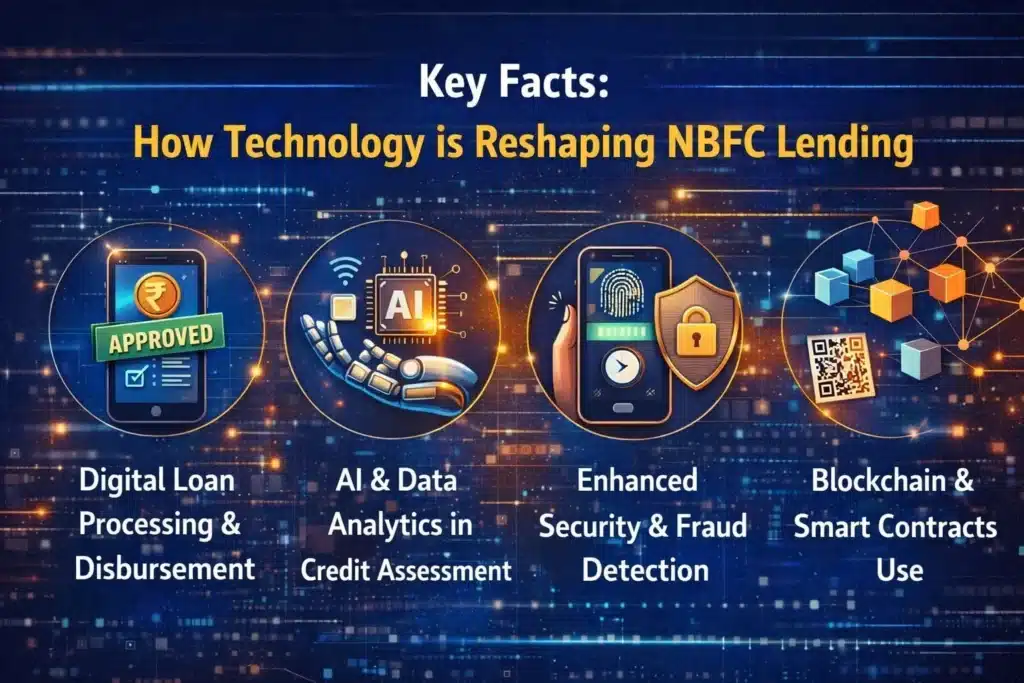

Key Facts: How Technology is Reshaping NBFC Lending

- Digital lending now makes up about 30% of total NBFC loan portfolios, compared to around 5% just a few years ago.

- FinTech-led NBFCs sanctioned ~10.9 crore personal loans amounting to ₹1,06,548 crore in FY 2024–25, reflecting accelerating adoption.

- Advances in AI and automation have reduced loan approval times from days to as little as a few hours (or even minutes).

- Co-lending models between NBFCs, fintechs & banks now account for ~30% of Indian digital lending.

- ~93% of lenders say ML has increased their loan-approval success.

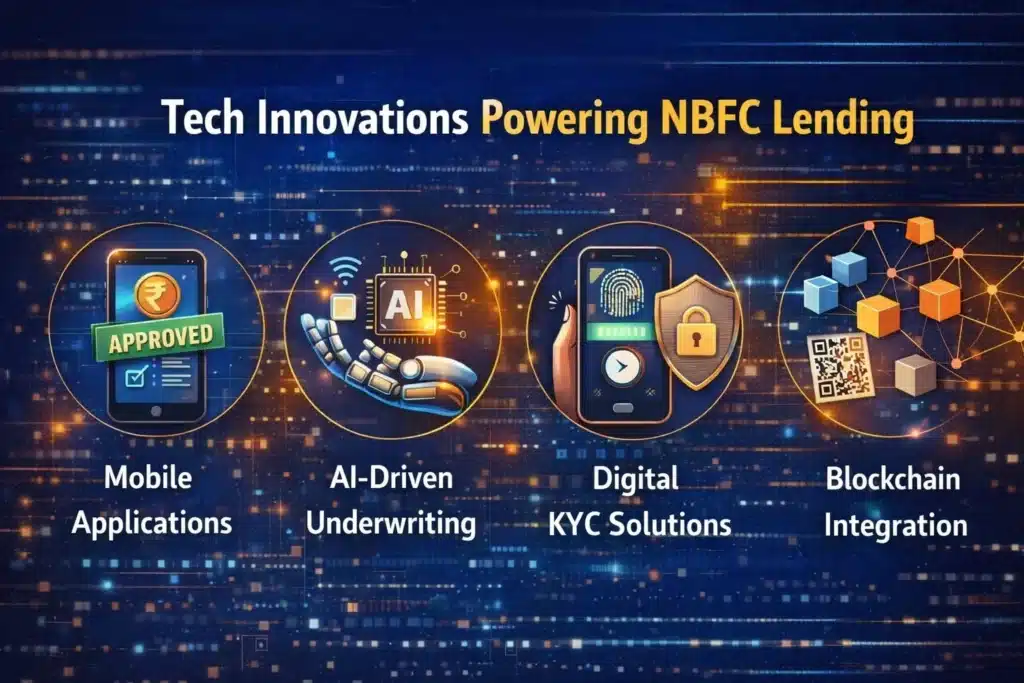

Tech Innovations Powering NBFC Lending

1. AI & Machine Learning for Smarter Credit Decisions

Credit underwriting is increasingly underwritten by AI and ML algorithms. Conventional credit scoring relies heavily on bureaus such as CIBIL scores. These days, sophisticated models crunch alternative data — ranging from digital footprints to UPI transaction histories, mobile usage patterns and even e-commerce behaviour — for a more inclusive and accurate indication of creditworthiness.

“With AI and ML, NBFCs are able to tailor credit offerings, while cutting down on time in approvals and enhancing the quality of portfolio.” – Industry Expert

2. Data Analytics & Predictive Modelling

Massive data tools analyse millions of pieces of information to predict risk, spot emerging trends and tailor loan products. These solutions support NBFCs in the delicate balance of risk and growth by providing real-time decisioning and predictive modelling of risk.

3. API-Driven Platforms & Digital Integrations

Open APIs are driving frictionless connectivity between lenders, credit bureaus, payment systems and third-party services, and fueling automated workflow from application through to disbursement.

4. Robotic Process Automation (RPA)

RPA eliminates the need for manual document verification and compliance checks, increasing operational efficiencies and avoiding mistakes.

5. Blockchain for Transparency & Security

Blockchain is under consideration for a secure, unalterable recording of loan records, adding transparency while reducing fraud and paperwork.

Table: Technology vs. Traditional NBFC Lending

| Feature | Traditional NBFC Lending | Tech-Enabled NBFC Lending |

| Loan Approval Time | 3 to 7 days or more | Minutes to 24 hours |

| Customer Onboarding | In person, paper-heavy | Digital eKYC & signature |

| Credit Scoring | Bureau data only | AI + Alternative data |

| Operational Costs | High manual effort | Automated & Cost-efficient |

| Fraud Detection | Manual rules | ML-driven proactive detection |

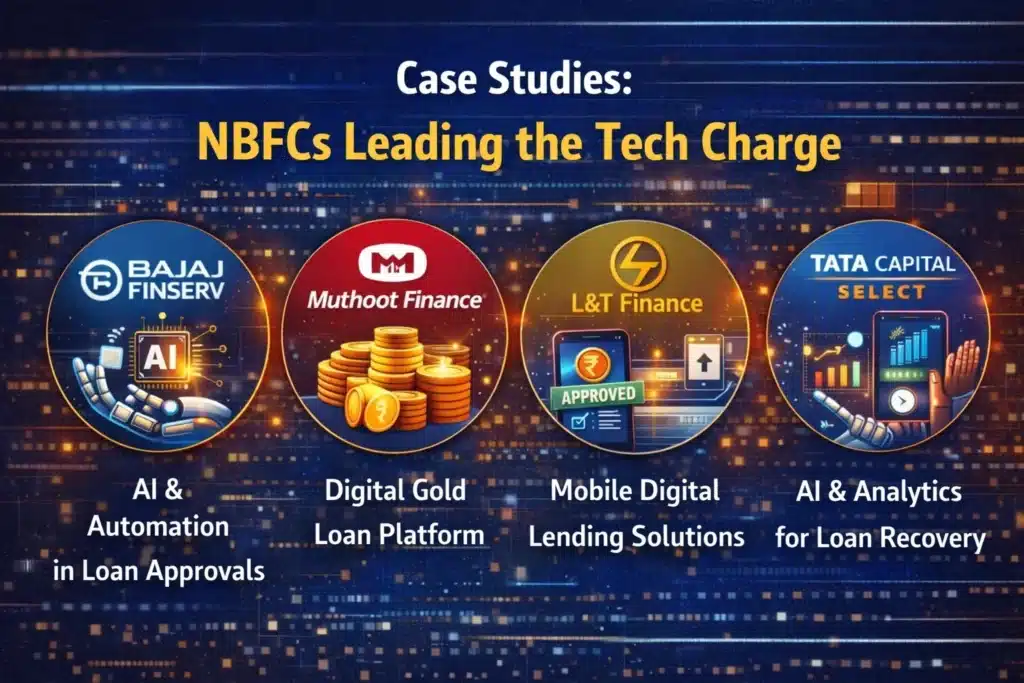

Case Studies: NBFCs Leading the Tech Charge

1. LendingKart – MSME Empowerment

LendingKart used cloud-based NBFC software combined with AI for credit analysis and went through over 5,000 borrower data points.

Impact:

- Loan approvals reduced from ~7 days to less than 24 hours

- Processed payments of over ₹12,000 crore to 300,000+ MSMEs in 4,000+ cities

- ~97% of onboarding is fully digital

“Automation in general allowed us to get into underserved markets rapidly — speed and reach working together.” – LendingKart Leader

2. Capital Float – Lending Embedded Everywhere

Capital Float, with its API-first approach, was able to integrate credit across platforms like Amazon Pay and Razorpay.

Impact:

- 5× increase in customer acquisition

- Loans worth Rs 7500 crore disbursed to 2.5 million customers

- ~85% of applicants approved within <15 mins

3. Indifi Technologies – Smart Sector-Focused Lending

Indifi plugs in live data for players like Swiggy and MakeMyTrip to measure performance, as well as creditworthiness, especially in segment-specific areas (like hotels).

Impact: Further penetrated targeted industry-wise MSME credit segments.

Emerging Trends & Strategic Shifts

Embedded Finance & BNPL Models

NBFCs are fuelling Buy-Now-Pay-Later (BNPL) services as well as micro credit at merchant platforms and wallets – transforming transactions to loans.

Co-Lending Partnerships

Banks with co-lending frameworks are responsible for bigger ticket loans and risk sharing — it’s a win-win of better capital access for borrowers, and compliance as well.

Regulator & Innovation Balance

As technology speeds up lending, the RBI has also warned that lenders should guard against excessive dependence on algorithmic credit models and diversify their funding and risk strategies — highlighting the need for prudent innovation.

Key Takeaways

- Tech powers speed: Digital processes, for instance, can shave the loan approval process from several days to minutes.

- AI & data are opening up financial borders for thin-credit.

- Integrations with fintechs and banks multiply reach and compliance.

- Blockchain & RPA are New Frontiers for Efficiency & Security.

Conclusion: A Digital Future for NBFC Lending

Now technology isn’t a mere enabler — it’s how NBFC companies lend, grow and serve India’s varied borrowers. From the AI-led lending scorecards to the API-driven ecosystem approach, tech is making NBFCs agile, inclusive and innovative lenders. Looking ahead, level-headed adoption of novel technologies — along with sensible policing — will be essential if growth is to continue.

Leading the charge in this digital transformation are innovators like Jaguar Software India that are helping NBFCs and financial institutions create scalable, secure, and intelligent lending platforms that help unlock faster decisions and deeper customer insights — guaranteeing businesses maintain their competitive edge in a thriving tech-powered lending ecosystem.

FAQs

What exactly are NBFC companies, and how are they different from banks?

NBFC (Non-Banking Financial Companies) are responsible for granting loans, credit facilities and financial services such as banking, but do not have a banking licence. NBFCs cannot accept demand deposits like savings accounts, unlike banks, but they often provide for faster approval, flexible requirement conditions and customised lending products, particularly to small businesses as well as to individual borrowers.

How is technology changing the way NBFC lending works in India?

Technology has literally transformed NBFC lending in India. Processes that used to take days can now be completed in minutes. With AI-driven credit scoring, digital KYC, data analytics and automation in place, they can sanction loans more quickly, travel light on the paperwork trail, cut down fraud, and even create customised loan products for borrowers with little to no history of borrowing.

Is digital lending by NBFCs safe for borrowers?

Yes, digital lending by regulated NBFCs is fairly safe when there is compliance with the norms. The majority of tech-enabled NBFCs are also secured on platforms which have encrypted data and RBI-prescribed KYC norms and fraud-detection tools. They must ensure that the NBFC is RBI-registered and work with transparent pricing and data-protection norms.

How does AI help NBFCs approve loans faster?

AI enables NBFCs to assess thousands of data points in real-time, from income patterns and transaction history to alternative sources of data like digital behaviour. This enables lenders to make more accurate risk decisions than the traditional underwriting process and approve loans in minutes, rather than days, without sacrificing credit quality.

Can people with low or no credit scores get loans from NBFCs?

Absolutely, that is one of the greatest benefits of technology-based NBFC lending. There are a lot of NBFC (non-banking financial companies) companies that are now utilising alternate data and machine learning models, so they can lend to new-to-credit customers, small business owners innovatively people in tier 2 and tier3 cities where the credit bureau does not necessarily have a rich record of all.

: A Global and Indian Perspective on Data Protection")